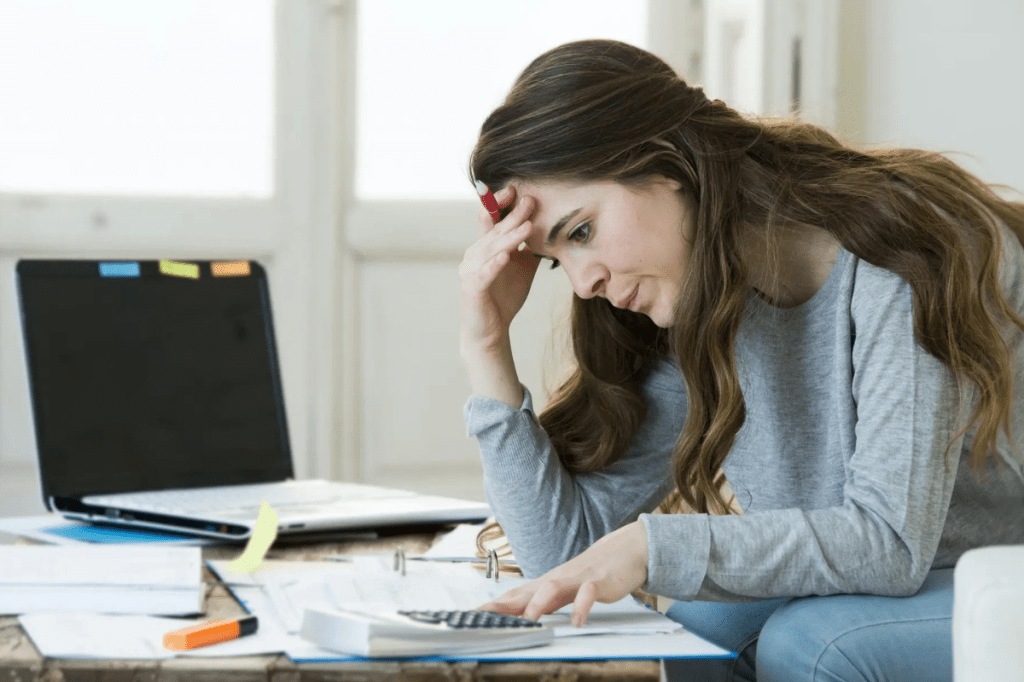

Falling behind on bills can happen fast. Here’s how to respond, protect yourself, and get support.

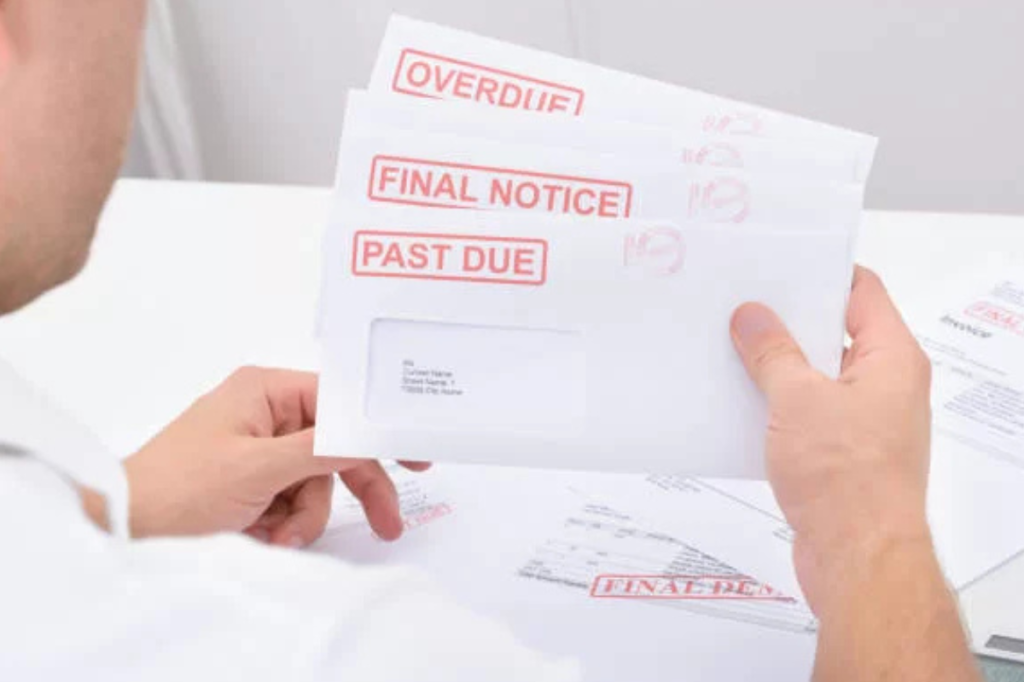

The phone rings. It’s a number you don’t recognise. You let it go to voicemail. The message is terse and official, asking you to call back urgently about an important financial matter. Your stomach drops. It’s a debt collector.

If that sounds familiar, you’re not alone. Thankfully, you’re not without options either. When bills pile up and debt collectors get in contact, most people’s instinct is to ignore, ignore, ignore. But that only leads to bigger problems.

Steffany Woolford from the South Australian Financial Counsellors Association says the stress of receiving debt collection letters and phone calls can feel very overwhelming and frightening – but it doesn’t have to stay that way. Knowing what to do next makes a big difference.

“There’s no shame in seeking support,” she says. “These things don’t discriminate; it can happen to anyone. The thing to keep in mind though is knowing that you’ve got options, and to act fast if it’s a secured debt (like a loan for a vehicle) as they can start repossession proceedings.”

Understand what’s actually happening

When you stop paying bills or repaying money you have borrowed, the money you owe becomes a ‘debt’. The business you owe money to, aka the ‘creditor’, will try to recover it. Sometimes they chase it themselves. Sometimes they have a debt collection agency chase the debt for them – or sometimes they will even sell the debt to a collection agency, often for less than the original amount.

That’s why you might suddenly hear from a company you don’t recognise.

“The important thing to know is that whether it’s the original creditor or a collection agency, the same rules apply – and those rules are there to protect you,” says Steffany.

Know your rights

Debt collection is legal. Harassment is not.

There are limits on how and when collectors can contact you:

- Between 8am and 9pm on weekdays,

- Between 9am and 9pm on weekends,

- No more than three calls per week and ten per month.

Turning up at your home is a last resort, and only allowed within those same hours. They cannot threaten you, use abusive language, or mislead you about what they can do.

“This surprises some people, but they can’t send you to jail or threaten to send you to jail just for owing a debt,” says Steffany. “Owing money is not a criminal offence. If a collector suggests otherwise, that’s a scare tactic – and it’s not allowed.”

That said, ignoring a debt does have real consequences. Creditors can list a default on your credit report, affecting your ability to get a loan, a phone plan or even a rental for years. For secured debts – like a car loan – they may be able to repossess the asset. They can also take you to civil court to recover what’s owed.

Steffany’s advice is to act, rather than ignore a debt, and get free legal advice if you are threatened by contacting the Consumer Credit Law Centre of South Australia on 1300 886 220.

“It’s all about knowing your rights,” Steffany says. “Knowledge is power – many feel pressured to agree to arrangements that aren’t sustainable, but with the right information and support, they can be offered a range of realistic options.”

Don’t go silent – start a paper trail

When those calls start, the worst thing you can do is disappear completely.

“You don’t need to have all the answers – but reaching out is important,” says Steffany. “If you do owe the debt, explain what’s happening and ask whether a hardship arrangement is available.”

“Over time, debt collection agencies have improved their practices and now have, or are introducing, policies focused on hardship and vulnerability, along with staff trained to provide support.”

Steffany says this means they may be able to offer more flexible options. “Don’t be afraid to make contact and explain your circumstance,” she says. “You might be surprised by the understanding and help that’s available.”

She also says it’s important to keep a simple record of every interaction: dates, times, who you spoke to and what was said. If you agree to anything, ask for it in writing. However, be careful what you put in writing as it may affect your statute of limitations on the debt.

If they cross the line – calling too often, contacting you outside permitted hours, or using threats – you can make a free complaint to the Australian Financial Complaints Authority (AFCA).

You don’t have to do this alone

If the calls feel overwhelming, or you’ve tried to sort things out and hit a wall, this is exactly what financial counsellors are for. You can find one near you here.

They’re free, confidential and completely non-judgmental. They’ll look at your full financial situation and help you work out a plan – including speaking to creditors to advocate on your behalf.

“When we contact a creditor for a client, we use the language of hardship and vulnerability,” Steffany says. “We know what to ask for, and creditors know they’re dealing with someone who understands the system. Sometimes that alone changes the conversation. It certainly helps to take a lot of stress off of you.”

“Many people say they wish they had contacted a financial counsellor earlier, as the support really reduced the pressure and worry.”

If you are on a wait-list to see a financial counsellor in person, Steffany suggests calling the National Debt Helpline for support – and to let creditors know you’re on a waiting list.

The government’s Moneysmart website also offers practical advice for getting on top of your debt, plus where to go for more information.

The South Australian Government offers free financial counselling that you can find through the Affordable SA website. Alternatively, contact the National Debt Helpline(1800 007 007) for free and confidential financial counselling, or the Mob Strong Debt Helpline for Aboriginal and Torres Strait Islander people (1800 808 488). See other cost-of-living options available to South Australians here.